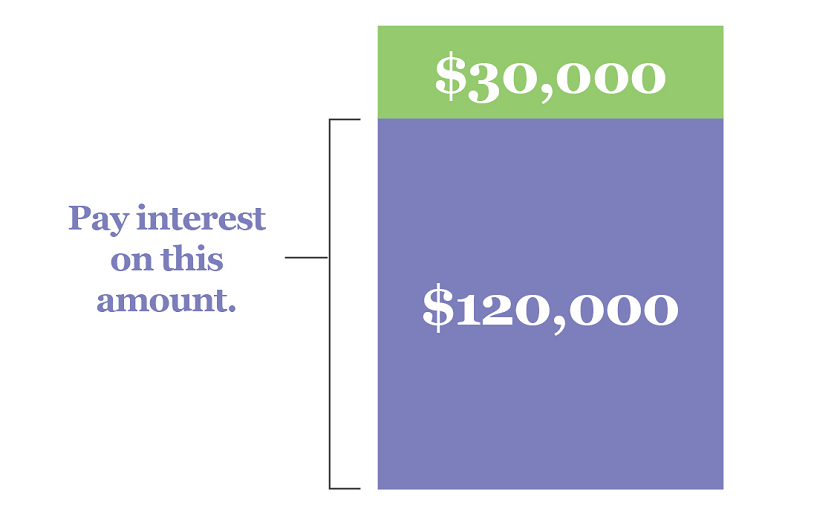

What is an interest-only home loan?

Making interest-only repayments on a home loan can make the cost more manageable as you’ll pay less each month. But this type of loan isn’t for everyone. We explain what’s involved.

One topic, zero jargon, in one minute.

Welcome to Home Loans 101 - a Defence Bank series of short videos that demystify and explain common home loan processes and terminology.

Choose a topic below then sit back and watch as our experts use clear and simple language to help guide you through your home loan journey.

Making interest-only repayments on a home loan can make the cost more manageable as you’ll pay less each month. But this type of loan isn’t for everyone. We explain what’s involved.

For homeowners, it's often better to make principal and interest repayments, where possible as it will save you time and extra interest costs.

Lenders mortgage insurance is a type of insurance that lets you buy a home with a deposit below 20%. This type of cover protects the lender, not the home buyer, so it’s worth looking at ways to cut the cost.

A home loan comparison rate includes the loan's regular interest rate as well as most upfront and ongoing fees, helping you make an ‘apples for apples’ comparison between different home loans.

Redraw is a feature of most variable rate home loans, letting home owners withdraw extra payments out of their loan if cash is needed in an emergency.

The loan-to-value ratio – or LVR – refers to the percentage of your home’s value you are borrowing through a home loan. The bigger your deposit, the lower your LVR – and the more you can save on loan interest.

Want to reduce the interest you pay on your mortgage? Here's how an offset account can do that.

If you’re looking to take out a loan, lenders are looking at one key piece of information: your credit score.

Building a new home - or completing major renovations to an established home - isn’t just exciting, it can also call for a different type of home loan called a construction loan.

You’ve saved a deposit, found a place you love, and now it’s time to apply for a home loan. We explain the paperwork you need to help your lender get the ball rolling without delay.

Buying a home involves more than paying a deposit. There are upfront costs that you need to budget for before you can turn the key to your dream property.

A fixed rate home loan can protect you from rising interest rates and extend the savings of low rates, but there’s a lot to consider before locking in your loan’s interest rate.

If saving a big deposit is holding you back from buying a home, don’t give up your goal. There are plenty of options to buy a house with less than 20% deposit.

A variable rate mortgage has an interest rate that may change over time and typically offers more flexibility than a fixed rate home loan.

Redraw and offset accounts both offer opportunities to save on home loan interest and become mortgage-free sooner. But there are key differences between the two. We weigh up how redraw works compared to offset.

Every lender has its own definition and requirements for genuine savings, which will depend on the amount that you borrow, and some may not even require it at all.

Home equity is the difference between the market value of a property and the outstanding mortgage balance.

From January 2023, there have been improvements to how ADF members and veterans can qualify for and access DHOAS, these are:

Portability of your Defence Bank DHOAS home loan may be possible if you don’t require additional funds to purchase your next home. Speak with a lender to discuss your situation further.

We also recommend you should always contact the Department of Veteran Affairs (DVA) before making any changes to your DHOAS home loan.

You and your partner will both need to be Defence Bank members to obtain a Defence Bank DHOAS home loan. The good news is that once you are a member, you will have access to our wide range of savings, investment, insurance and loan products.

Talk with one of our home loan consultants to discuss how we can assist you.

You and your partner will both need to be Defence Bank members to obtain a Defence Bank DHOAS home loan. The good news is that once you are a member, you will have access to our wide range of savings, investment, insurance and loan products.

Talk with one of our home loan consultants to discuss how we can assist you.