The idea of paying interest-only on a home loan can be very tempting. However, there are pros and cons to weigh up, and interest-only may not be the best choice for you.

To be clear, interest-only loans aren’t a separate type of home loan. The same basics apply in regards to the loan having a set term and either a fixed or variable interest rate. Rather, the difference lies in the loan repayments. With an interest-only loan, your regular repayments are made up of nothing more than interest charges. There is no repayment of the loan itself.

That’s quite unlike the more traditional ‘principal and interest’ repayments, where each monthly payment is comprised of both interest plus a small repayment of the loan balance. In this way, you steadily chip away at the loan each month, and at the end of the loan term, the balance is paid off entirely.

Lower monthly repayments.

As the regular payments on interest-only loans don’t include any repayment of the loan balance, the monthly payments are lower. This can mean having more to spend each month on other living costs, or having extra cash to pay down other debts with a higher interest rate.

The catch is that with interest-only payments you won’t make any inroads into the loan balance. Even after years of making interest-only payments, you’ll still owe the same amount as when you first took out the loan.

This explains why most homeowners prefer to make principal and interest payments. It may cost a bit more each month compared to interest-only payments, but it means that the loan is being steadily paid off over time. This helps to boost a home owner’s equity in their property, and it ensures that further down the track the homeowner will own their place mortgage-free.

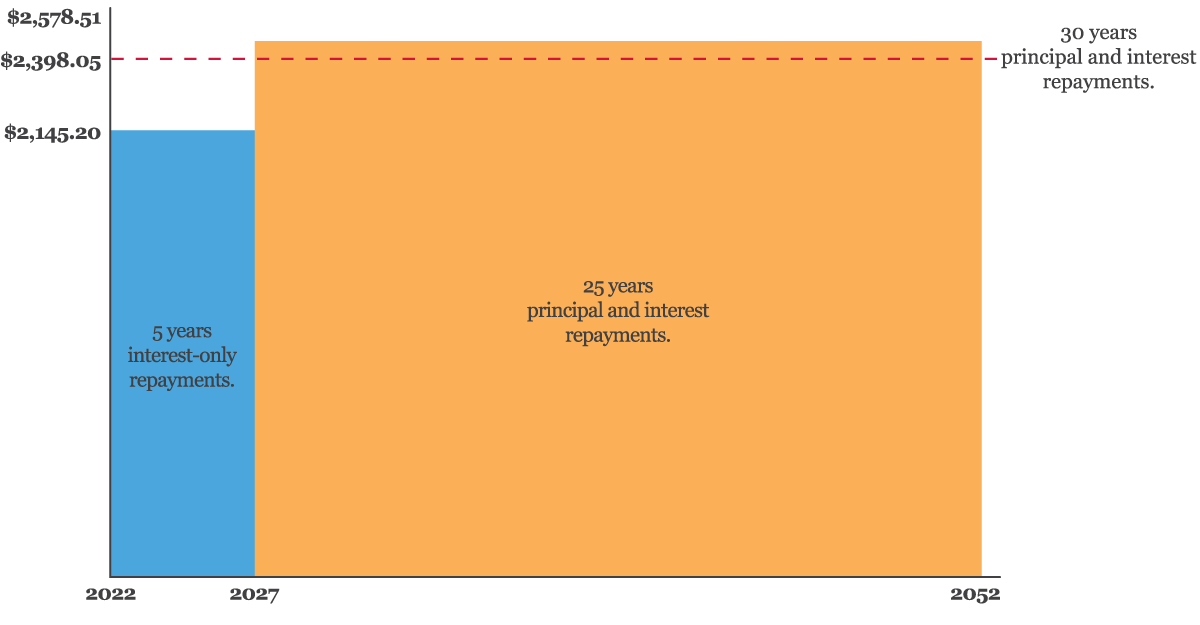

By way of example, Bruce has taken out a home loan of $400,000 for 30 years.

If he were to make principal and interest repayments:

- At 3.47% p.a. from year one, his monthly repayments would be $2,398.05.

If he decides to make interest-only payments:

- For the first five years of his loan at 3.82% p.a., his monthly payments would be $2,145.20.

- In year six, his payments would revert to principal and interest at 3.47% p.a. with monthly repayments increasing to $2,578.51.

To help you calculate what your repayments might be on an interest-only home loan use our repayment calculator.

Why interest-only appeals to investors.

For investors, making interest-only payments can hold plenty of appeal. It means less money spent on the property each month, which is a plus for cash flow.

In addition, an investor may only plan to hold onto a property for a short period before reselling it for a profit. When that happens, the loan can be repaid in full as soon as the property is sold.

Australia's Defence Bank offers interest-only payments across a number of Defence Bank investment home loans.

Interest-only payments don’t last forever.

Most lenders only permit interest-only payments for a set period – often a maximum of five years. After that, you’ll need to re-apply to the lender to continue making interest-only payments, or start making principal plus interest payments.

The verdict.

An interest-only home loan can be useful as a temporary option for homeowners who are facing a reduced income for a limited period – such as taking parental leave for the arrival of a new baby. In general, though, making principal plus interest repayments is the preferred choice for homeowners as it will mean owning the home debt-free at the end of the loan term.

For investors, an interest-only loan may help to maximise the tax deductions on a rental property. That’s because only the loan interest can normally be claimed on tax, not the repayment of the loan principal. However, we recommend you should seek independent professional tax advice on this matter.

The law requires us to give you information about how we use any personal information we collect from you. Please read our Privacy Policy.

Important note: This information is of a general nature and is not intended to be relied on by you as advice in any particular matter. You should contact us at Defence Bank to discuss how this information may apply to your circumstances.