Nothing beats the feeling of walking into a brand new home that’s all yours! You have the freedom to choose your block of land, your style of home, and of course, there’s the excitement of watching your new home take shape from the ground up.

Building a new home - or completing major renovations to an established home - isn’t just exciting, it can also call for a different type of home loan called a construction loan.

A traditional home loan makes the funds available to you as a single lump sum. By contrast, with a construction loan, funds from your loan are released in stages as construction progresses which is known as ‘progress payments’.

These ‘progress payments’ are used to pay your builder, and it’s a system that works in a home owner’s favour as interest is only charged on the funds drawn down. This way, your repayments start out small, and gradually increase as construction nears completion.

Applying for a construction loan.

The process of applying for a construction loan is similar to a regular home loan. But some important differences apply.

Your lender will want to see evidence of your income, some personal ID, and other details about your regular spending and savings history to know you can comfortably manage the loan.

You’ll also need some extra paperwork. This is because you’re asking the lender to fund an asset (your home or renovation) that doesn’t yet exist. As a guide, the additional documents a lender will ask for include:

- A copy of the fixed price building contract showing all the specifications and costs.

- A copy of any contract variations (where you have requested the builder vary the original plans).

- Evidence of approval of your building plans by your local council.

- Evidence that the builder is licensed and insured.

- A copy of the home warranty insurance certificate.

The timing of progress payments.

When your construction loan is approved and any deposits paid, your builder can start to get to work. The loan funds will be drip-fed to the builder via progress payments that coincide with various construction milestones. These stages should be set out in your building contract.

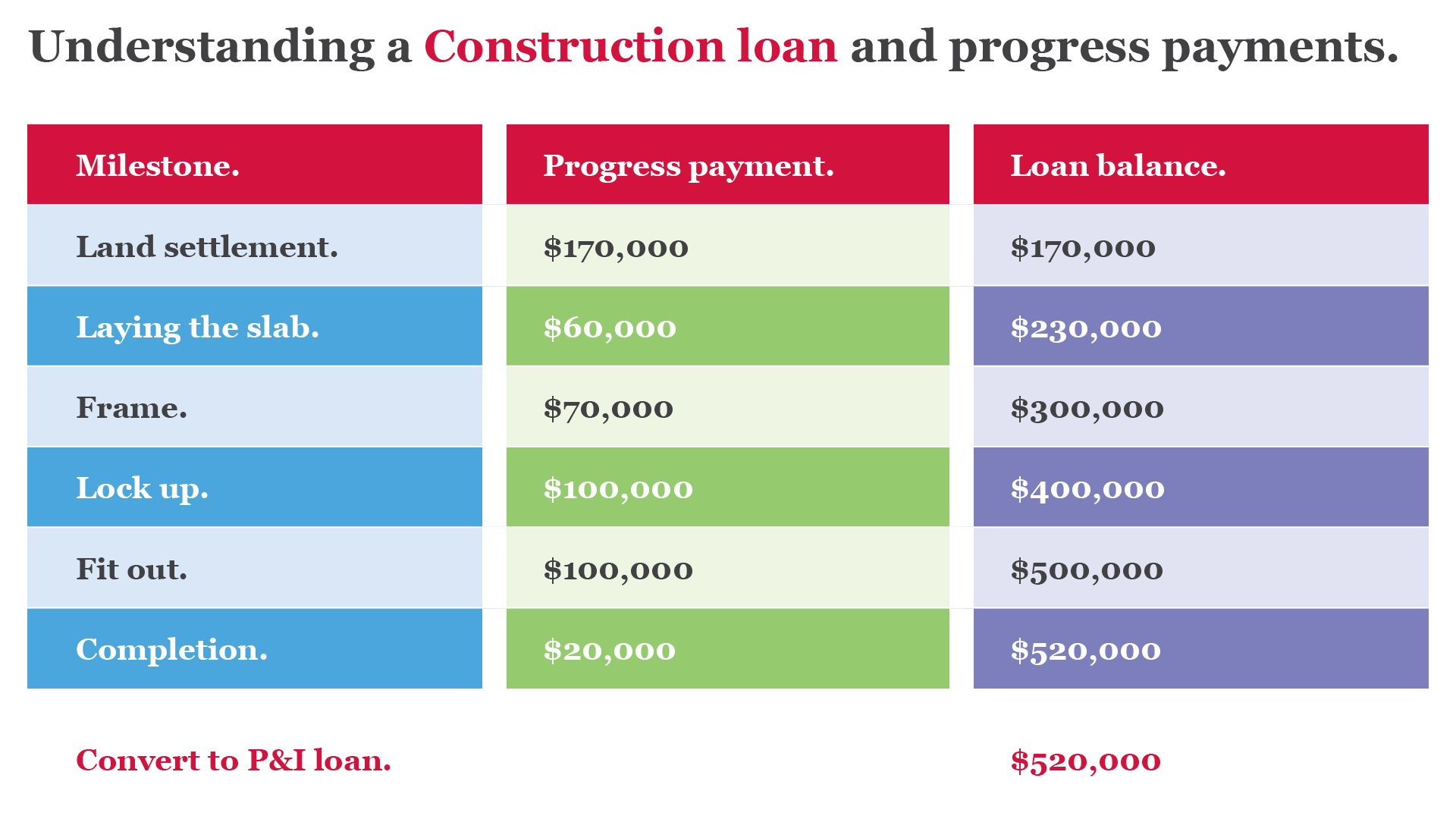

The progress payments are usually made at six main stages of construction:

- Land settlement: This is for the purchase of the land you are building on.

- Laying the slab: This stage sees the concrete slab (or pad) poured that your home will stand on.

- Frame: During this stage the wall frames and roof trusses will be erected, giving you a glimpse of what your home will look like.

- Lock up: This is when your home really takes shape, with brickwork completed and the roof in place. Once windows and doors are fitted, your home will be weatherproof, and can be securely locked at the end of each working day.

- Fit-out: This is where the interior of your home is fully kitted out – the kitchen, bathroom and laundry will have functioning features, the walls will be painted and floor coverings laid.

- Completion: At this point construction is complete. The council will want to visit and inspect your home, and your lender may also visit to ensure your home is built to a high standard.

What happens when your home is complete?

There are plenty of inspections to be made and signed off before you can move into your new home. But once construction is complete and progress payments have been finalised, your loan will no longer be a construction loan.

Instead, it will become a traditional home loan that sees you making regular principal and interest repayments as you settle into life in your newly built home.

The law requires us to give you information about how we use any personal information we collect from you. Please read our Privacy Policy.

Important note: This information is of a general nature and is not intended to be relied on by you as advice in any particular matter. You should contact us at Defence Bank to discuss how this information may apply to your circumstances.