- Defence Bank records net profit after tax of $13.9m for FY 2020/21, up by 38%.

- Deposit growth of 5.7%, total deposits of $2.3b.

- Lending growth of 8.0% with total loans of just under $2.5b at 30 June 2021.

- Capital adequacy reaches a four year high at 16.0%.

- Loan delinquency rate remains low, at just 0.08%.

- Return on assets is 0.49%, with return on equity at 7.11%.

Defence Bank today recorded a 38% increase in profit, fuelled by record lending.

“Our people led and technology-enabled strategy has delivered these results for our members,” Defence Bank CEO David Marshall said.

“We’ve invested in our team and in digital advancement to foster effortless banking, allowing our people to deliver an authentic, easy-to-navigate, personalised banking service.

“We have provided stability, consistency and convenience to our members against the backdrop of uncertainty and rapid change caused by the COVID-19 environment.

“Our fundamentals are strong, our return on assets is 0.49%, our return on equity sits at 7.11%, and our net interest margin has lifted from 1.84% in FY 2019/20 to 1.98% in FY 2020/21.

“Total deposits have grown by 5.7% to $2.3B for FY 2020/21.

“We have responded to our member’s appetite for banking that’s convenient, requires minimal effort, and is compatible with their busy daily lives.

“Members love our Defence Bank app, as shown by a rating of 4.8 out of 5 in the App Store, well ahead of our competitors.

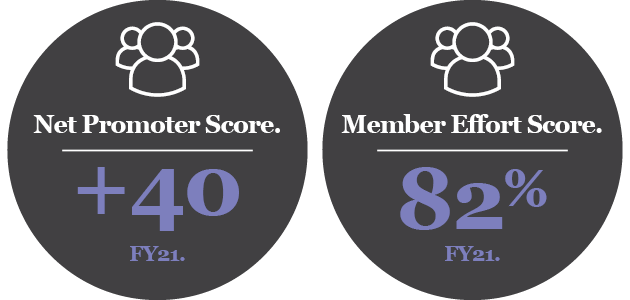

Feedback like this from our members is so important and we have thousands of members happy to recommend Defence Bank and telling us it’s easy to bank with us. Defence Bank recorded an average Net Promoter Score of +40 and a Member Effort Score of 82% during the year, well ahead of the big four.

“Defence Bank is extremely well capitalised, recording capital adequacy of 16%, the highest for the bank since 2017. Our inaugural $15M subordinated notes transaction and $300M capital relief public RMBS transaction both added significantly to this result.

Our cost to income ratio has also improved, moving from 73% to 69% in 12 months.”

During FY 2020/21, Defence Bank reached $3Billion in assets, and received a rating of Baa1 | Stable | P-2 from Moody’s Investor Services due to strong asset quality, good capitalisation and profitability. The recognition from Moody’s provides a dual rating for the Bank, with a rating of BBB |Positive|A2 re-confirmed by S&P Global Ratings during the financial year.

Marshall said while uncertainty remains in the COVID-19 environment, Defence Bank is well placed for continued growth and refuses to use Covid as an excuse not to do so.

“We expect continued demand for all of our products and services.

“This includes continued demand for home loans, particularly from younger members. We remain prudent lenders who want to get more Australians into homeownership but not by getting them in over their heads. Our overall loan delinquency remains very low, at just 0.08%.

“As regulators take a renewed focus on serviceability, Defence Bank is well placed to easily meet these and any further requirements.

“Our focus continues to be on accelerating improvements in our member experience with more digital banking investment a key priority over the next 12 months.”